1. Executive Overview

Aye Finance Limited is a Non-Banking Financial Company – Middle Layer (NBFC-ML) focused on providing loans to underserved micro and small businesses (MSMEs) in India. Since starting operations in 2015, the company offers secured and unsecured small-ticket loans for working capital and business expansion across sectors like manufacturing, trading, services, and agriculture.

As of September 2025, Aye Finance has an AUM of ₹60,276 million, with strong growth over recent years. It serves over 5.8 lakh customers through 568 branches across 18 states and 3 union territories. With a small average loan size (~₹0.18 million), the company ensures better risk diversification. Its key strengths include wide geographic presence, fast growth among peers, and a unique “phygital” model combined with cluster-based lending, which helps maintain strong customer retention and stable asset quality.

2. Business Model and Revenue Streams

Aye Finance employs a localized, direct-to-customer "phygital" business model, entirely eliminating reliance on Direct Selling Agents (DSAs). Revenue is driven by high-yielding lending products originated via a massive in-house workforce of over 3,905 loan officers and 1,019 relationship officers.

- Geographic Breakdown: The portfolio is systematically diversified across four zones: North (34.80%), East (27.79%), West (22.73%), and South (14.69%) as of H1 FY26. The top five states (Bihar, Uttar Pradesh, Rajasthan, Madhya Pradesh, and Maharashtra) collectively contribute 57.00% to the overall AUM.

- Pricing Strategy & Spreads: The company commands significant pricing power, generating an annualized Yield of 25.39% for H1 FY26 (down from 26.53% in FY25) while maintaining an Average Cost of Borrowing of 11.64%. This spread allows for an exceptionally strong Net Interest Margin (NIM) of 14.12% in H1 FY26 (15.31% in FY25).

- Operational Metrics: The company exhibits strong unit economics. AUM per Branch stands at ₹106.12 million, and the Cost to Income Ratio has fundamentally improved, dropping from 66.03% in FY23 to 52.62% in H1 FY26. Furthermore, Repeat Retention Rate sits at a healthy 41.16% for H1 FY26, significantly lowering customer acquisition costs (CAC).

3. Products and Service Portfolio

Aye Finance provides a comprehensive suite of secured, partly secured, and unsecured credit facilities tailored to businesses with annual turnovers between ₹2.00 million and ₹10.00 million.

- Secured Hypothecation Loans (Primary Revenue Driver): Accounts for 41.01% of AUM (₹24,719.26 million). Fully secured by hypothecation of working assets, machinery, and finished goods. Offers an ATS of ₹0.15 million over ~29 months, yielding up to 32% p.a..

- Unsecured Hypothecation Loans: Contributes 37.97% to AUM (₹22,888.82 million). Partly secured against hypothecation but where asset value cannot fully cover the loan. Yields up to 32% p.a. with an ATS of ₹0.17 million over ~31 months.

- Mortgage Loans (Growth Driver): Accounts for 19.28% of AUM (₹11,620.40 million). Fully secured against property. Targeted for up-selling, it offers larger ticket sizes (ATS ₹0.41 million), longer tenors (~75 months), and competitive pricing up to 26% p.a..

- 'Saral' Property Loans: Niche product comprising 1.74% of AUM. Tailored for clients with unclear property titles; ATS ₹0.19 million, yielding up to 28% p.a..

- Emerging Digital/Ecosystem Products: Includes SwitchPe, a B2B supply chain finance app offering unsecured credit lines with 14-day interest-free periods to retailers/distributors, and Shakti Loans, specifically targeting women micro-entrepreneurs.

Product-Wise AUM Breakdown (FY23 - H1 FY26)

| Product Category | FY23 AUM Mix | FY24 AUM Mix | FY25 AUM Mix | H1 FY26 AUM Mix (Sep 2025) |

|---|---|---|---|---|

| Mortgage Loans | 1.86% | 7.50% | 14.72% | 19.28% |

| 'Saral' Property Loans | 4.27% | 2.65% | 1.98% | 1.74% |

| Secured Hypothecation Loans | 63.60% | 51.94% | 43.62% | 41.01% |

| Unsecured Hypothecation Loans | 30.26% | 37.91% | 39.68% |

4. Key Business Strengths

- Large Market Opportunity: Targets India’s huge MSME credit gap (~₹34 trillion), a segment largely ignored by banks.

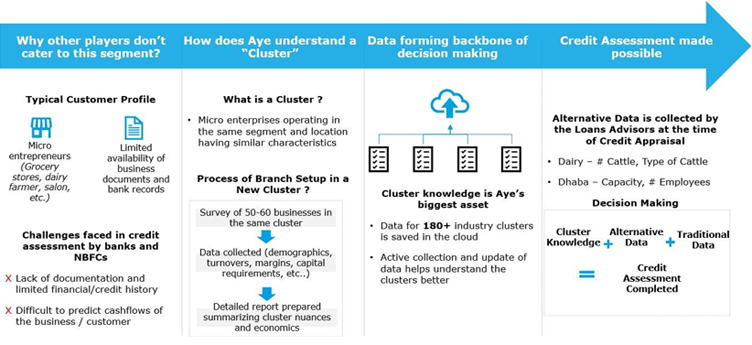

- Unique Underwriting Model: Uses a “business cluster” approach instead of traditional documents to assess borrowers.

- Strong Risk Diversification: Well spread across states, reducing risk from regional issues.

- In-House Sourcing: No agents used, ensuring better loan quality and higher customer retention (~41%).

- Good Asset Quality: Strong collection system and tech use keep bad loans low (Stage 2 ~1.65%).

- Diversified Funding: Supported by 80+ lenders with strong capital position (CRAR ~32%), enabling lower borrowing costs.

5. Future Growth Strategy

- Increase Branch Productivity: Focus on growing loan book in existing branches instead of rapid expansion.

- Expand Mortgage Loans: Increase higher-value, long-term loans by cross-selling to existing customers.

- Use AI & Automation: Improve efficiency and reduce costs using AI, RPA, and automated loan processing.

- Lower Cost of Funds: Shift towards better lenders and cheaper funding sources to maintain strong margins.

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.

Discussion

Join the discussion!

Log In to CommentNo comments yet. Be the first to share your thoughts!